Chris IggoAXA IM Chief Investment Officer, Core Investments

December 1, 2021

Investment Strategy outlook 2022: Coping with modest rate increases

COVID will remain an issue for markets; however, inflation is more of a concern. Modest interest rate increases in some economies need to be built into the investment outlook; however, a lot is priced in. If actual moves are in line, then bond market losses need not be significant. Equity markets can cope with modestly higher rates so long as earnings keep growing.

7 minutes

Read Outlook 2022 full article

DownloadOriginal Content: AXA IM

Inflation brings focus on low bond yields

As we head towards the second anniversary of the outbreak of the COVID-19 pandemic the disease remains one of the key worries for investors. It continues to have the ability to disrupt demand and supply and for this to be reflected in bouts of risk-off

behaviour in financial markets. Typically, unexpected shocks tend to raise questions about the ability of the global economy to sustain its pace of recovery. This in turn triggers buying of assumed safe-haven assets, generating counter-intuitive moves in bond yields when the macro narrative is one of inflationary growth and higher interest rates.

The coming year is likely to see this pattern of market behaviour continue. However, while COVID will remain an issue, the increase in inflation rates around the world is likely to be the key concern. Policy makers dealt with the potential impact of COVID on the global economy by aggressively cutting interest rates and loosening fiscal purse strings. This first supported and then boosted economic growth and was reflected in higher valuations for corporate assets. The remedy for inflation is not so benign. Central banks have been trying to increase inflation in recent years and are now faced with potentially having to reduce it. To do that, interest rates will need to go up in several economies and that will have very different implications for bond and equity market returns, and economic growth.

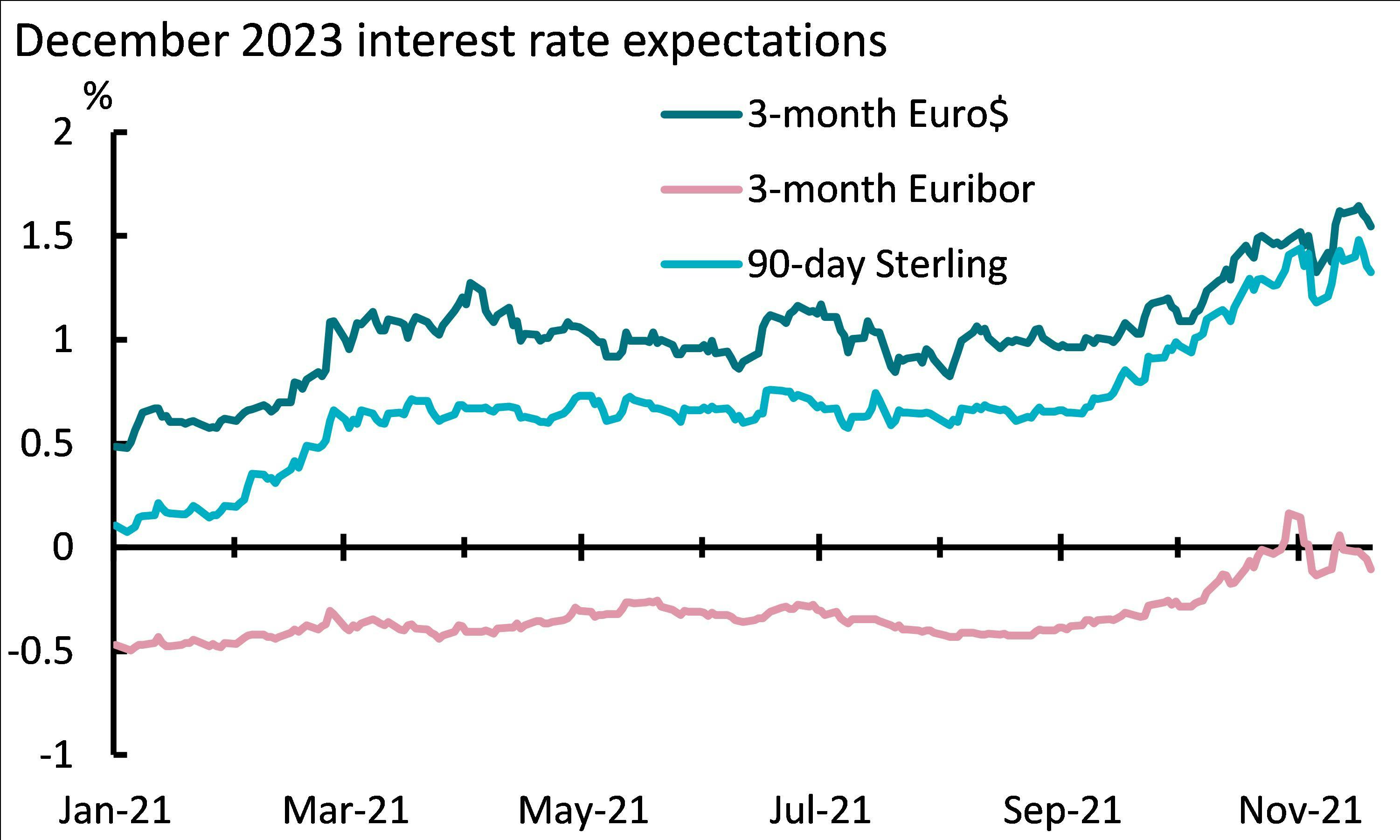

Through the second half of 2021, markets have increasingly priced a higher probability of interest rates going up. The rapid increase in inflation rates drove these expectations and allowed them to become dislodged from the prevailing forward guidance that central bankers had used as one of their post-crisis monetary policy tools. Looking to 2022, investors need to contemplate a number of issues over the likely trajectory of inflation itself, whether central banks will need to do more than what is already priced in, and how portfolios should be adapted to hedge against a worse outcome. That worse outcome would be even higher inflation, a more aggressive tightening of monetary policies and a subsequent downgrade to growth prospects.

Exhibit 1: Rate expectations move higher

Source: Bloomberg and AXA IM Research, 19 November 2021

Our base case scenario on inflation described in the 2022 Outlook is consistent with what is priced in bond markets. So far, that has prevented a significant increase in long-term yields which, in turn, has allowed equity markets to deliver strong returns. Yet several major central banks could start to increase policy rates from their pandemic-crisis levels over the next year or so. These moves would start from very low levels and, if market assumptions are correct, would be limited in nature. However, the era of pandemic-crisis monetary policy is coming to an end.

As we approach the shift in the stance of monetary policy globally it is important to consider different scenarios and how they will impact on different return expectations across asset classes. A negative bond and then equity shock would only come if it appeared that policy makers were changing their long-term equilibrium rate views. If incoming data pushes the Federal Reserve to concede that its terminal policy rate is not 2.5% but something higher, long-term bond yields and, importantly, real yields could move significantly above levels seen in the market over the last two years. That would undercut growth and earnings momentum. Negative returns in bonds would quickly be followed by large corrections across equity markets.

In the 1980s, it was the unexpected decline in inflation that drove real returns higher. There is a risk that the opposite situation is seen in 2022-2023. However, for now this remains a risk rather than the central expectation. Inflation is likely to be transitory even if elevated rates persist well into 2022. The idea of reverting to wage-price spirals in the US and other major economies appears somewhat fanciful. If we are right on that, bond markets can cope with some modest tightening so long as inflation does appear to be receding. A 100 basis points or so of higher rates would not be cataclysmic for equity investors who have been rewarded for being in an asset class driven by super-charged earnings. Slightly higher rates and a little easing in earnings growth across equities is hardly the stuff of bear markets. Ongoing recovery, innovation around climate change and re-purposing supply chains should be strong tailwinds for equity investors for some time.

However, some insurance in portfolios is not a bad thing. Inflation linked bonds have outpaced actual inflation in this cycle and should continue to do so in 2022. Other fixed income assets will struggle but even then, actively managed duration and credit exposures can deliver positive returns for investors. It is worth keeping in mind that it is very rare to get two consecutive years of negative returns in developed government bond markets. Forecasts of significantly higher bond yields have been wrong in the past - they could be wrong again. On the equity side, firms with less leverage, with strong pricing power and innovative product lines will prosper.

Very low interest rates and central bank quantitative easing have been the norm since the Global Financial Crisis in 2008-2009. As the world economy exits the pandemic period, central bankers are rightly adjusting the policy mix. We will see less bond buying and a gradual normalisation for rates. Many financial market commentators have all too easily made the link between loose monetary policy and signs of excess in financial markets. Yet to get very bearish on markets we would need to believe the following. Risk-free rates will rise as central bank interventions subside; this will have some portfolio re-balancing effects as investors move back out of risk assets into government bonds; and risk premiums will need to rise in credit and equities to reflect a more uncertain economic outlook in a world where central banks are less active.

In short, if monetary support is removed too quickly, the business cycle becomes shorter as tighter conditions in the short to medium term lead to a slowdown in growth. The extent to which this could happen really depends on inflation. The impact of the pandemic on global economic trends – supply disruptions, potential long-term changes to supply chains (just-in-case replacing just-in-time), labour markets and fiscal policy – will take some time to really understand. For now, however, central banks will err on the side of caution and will need to be convinced – by evidence of persistent second round effects – that the decades long period of low inflation is coming to an end. In the meantime, investors should still enjoy decent returns as companies continue to respond to structural forces like digitalisation and the energy transition.

On that final point the progress towards decarbonisation will increasingly determine capital allocation and investment opportunities. Investors are playing a key role in supporting de-carbonisation through asset allocation decisions, in engagement with companies on transition plans, and by supporting new technologies and business models that rate highly in terms of Environmental, Social, and Governance (ESG). Energy prices rose in the second half of 2021 – a key reason why broader inflation has also increased – yet, there has been no global approach to pricing carbon, which could push energy prices even higher. When it comes, and it will, the economics will swing sharply in favour of renewably produced energy and that will quickly allow upstream activities to benefit. Investors will be faced with opportunities to profit from the growth that will stem from this.

Price increases will be a necessary part of the energy transition, but it need not be something that brings back significantly higher interest rates and more macroeconomic

volatility. In 2022, investors will be keenly focussed on the peak in inflation and how insidious it’s impact on pricing and wage behaviour will be. The bullish scenario is that inflation will peak, and the flexibility of the modern, still very interconnected global economy will allow expectations to once again be firmly anchored. This would be the distinction between relative and general price adjustments in this context of internalising carbon in a range of production processes and should continue to present central banks with broad room for manoeuvre in delivering their inflation mandates. However, when many prices make relative adjustments, they create a general adjustment – or inflation - and that could challenge investor confidence in medium-term low inflation economies.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.