Commitments

AXA EssentiALL: Inclusive insurance

Empowering customers living on modest incomes around the globe to better protect their families, businesses and communities.

As an insurer committed to making a positive impact, AXA continues to take action to reduce insurance inequalities worldwide. Today, 70% of the population in emerging economies and more than a quarter of Europeans are either unable - or no longer able - to access insurance products and services. As a leading global insurer, we are determined to help close this protection gap by developing inclusive insurance solutions for modest-income customers, who are increasingly exposed to risk and the economic consequences they entail.

Meet Moustapha, one of AXA EssentiALL’s customers from Senegal

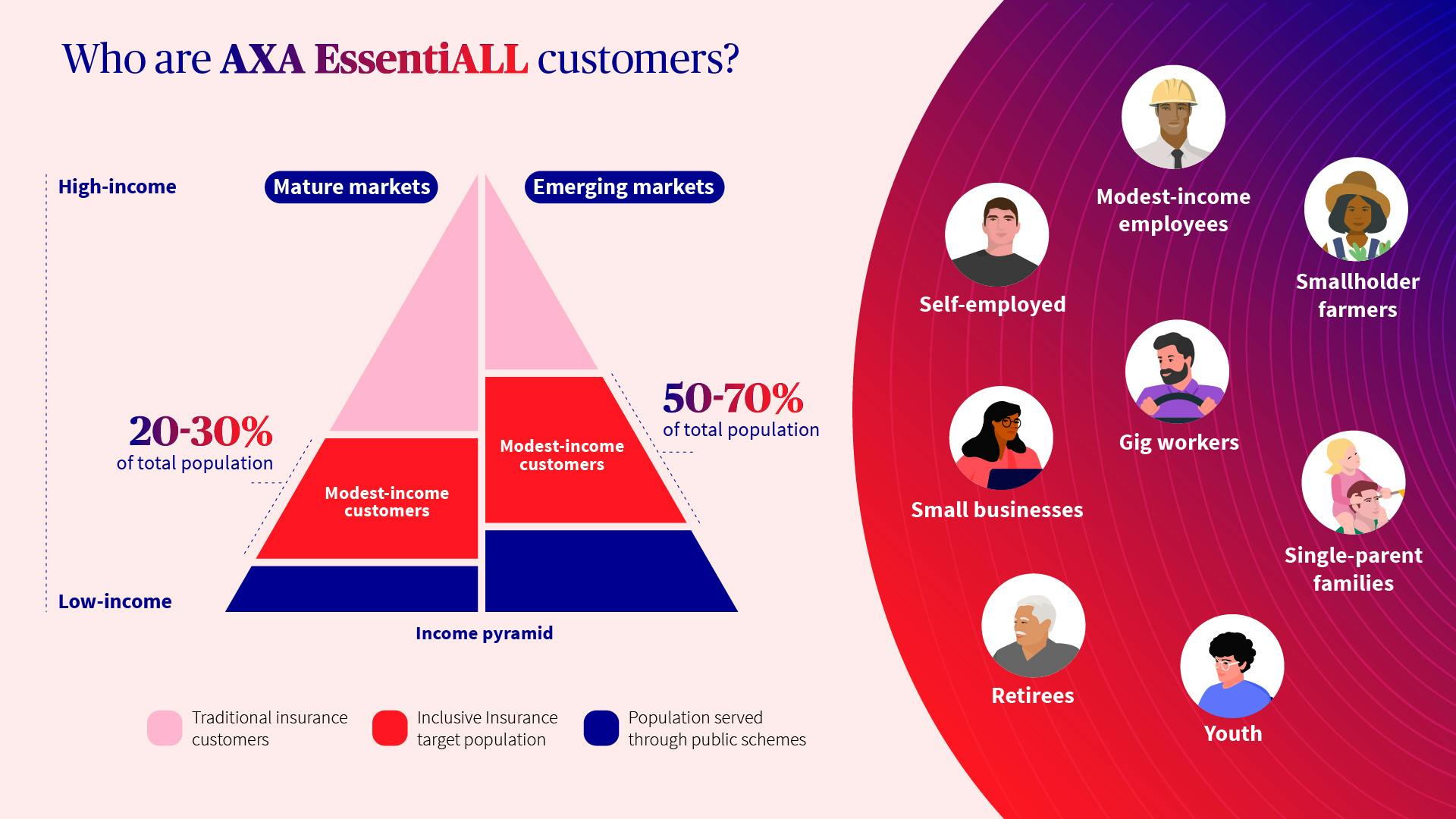

AXA EssentiALL brings inclusive insurance to modest-income customers across 21 countries, in both mature and emerging markets. Our customers are small business owners, microentrepreneurs, gig workers, farmers, young people, and retirees. What they have in common is that they have to navigate their daily lives on limited or highly volatile incomes making them even more vulnerable when facing unexpected financial shocks in their families, communities, or work. Damage to a vehicle can put a gig worker’s livelihood on the line, and medical emergencies frequently force families to take on debt they struggle to afford.

Helping customers manage these risks requires reinventing the way insurance is done, and AXA has been doing so for a decade. AXA launched its inclusive insurance business unit in 2016, originally named AXA Emerging Customers, to cover the essential insurance needs of low- to middle-income households and small businesses in emerging markets. In 2024, under the new name ‘AXA EssentiALL’, it extended its geographical scope to Europe in response to an increasing need: families on modest incomes are facing higher degrees of uncertainty, decreasing purchasing power, and declining standards of living.

Today, AXA is the only global insurer committed to inclusive insurance in both Emerging and European markets. AXA EssentiALL inclusive insurance is a sustainable and a profitable business at the heart of AXA’s 2024-2026 strategic plan, “Unlock the Future”.

Key figures for 2025

Ambition for 2026: On track to reach over 20 million customers

Garance Wattez-Richard

CEO of AXA EssentiALL

Insurance is the only financial service fully dedicated to managing unexpected shocks - shocks that often push modest-income populations into poverty or prevent them from ascending the socio-economic ladder. Through its insight-based offerings, AXA EssentiALL empowers customers with modest revenues worldwide - individuals and businesses alike - in order to help them make ends meet at the end of the month. In other words, it contributes to securing their financial health.

Reinventing insurance: An inclusive business model in practice

Adapting insurance to the needs of modest-income customers requires reinventing our business model to overcome the barriers faced by our customers. These include high costs and a lack of access, as well as limited understanding and trust in insurance. To do so, we provide solutions based on the ‘3A’ principles of inclusive insurance that are:

Affordable: we focus on clients’ essential needs, taking out unnecessary requirements, while introducing flexible payment facilities compatible with customers’ cash flows.

Attractive: we design inclusive insurance solutions that meet the needs and aspirations of our customer segments. The customer journey from policy issuance to claims is adapted to the segment’s preferences – whether physical, digital, or both – offering simplicity and convenience.

Accessible: we distribute inclusive insurance products through channels that are trusted by modest-income customers and small businesses. These include microfinance institutions, local MSME banks, farmer cooperatives, mobile phone network operators, digital platforms, and retailers, but also employers and public-private partnerships.

Propositions are co-created with customers and distributors to ensure that both the product and delivery methods are tailored to customer needs. The distribution strategy is defined for each market based on local market practices and AXA’s positioning. For instance, with Compagnie Nationale d’Assurance Agricole du Sénégal (CNAAS), AXA EssentiALL delivers a comprehensive health, life, and accident coverage to 300 smallholder farmers in rural and hard-to-reach areas via cooperatives and local village leaders. Further, in Mexico, AXA provides life insurance to over 240,000 teachers of public primary education through member associations. By doing so, we can reach communities with modest incomes, enabling them to build resilience and work towards improved financial health.

AXA’s inclusive insurance business at a glance

Our customers face a wide range of risks to their lives, families, and businesses. AXA EssentiALL develops insurance solutions designed to meet their essential needs:

- Protecting our customers and their families (Protection and Health) - 50% of AXA EssentiALL customers (10.3 million)

Protection insurance solutions are life insurance products covering family livelihoods in case of death, accidents, or disability of a breadwinner. Health insurance aims to limit out-of-pocket expenses and compensate the loss of income derived from unexpected health-related conditions. In several markets, we provide additional services that help customers manage their everyday health needs.

For example, in France, we offer “Ma Protection pour votre Commune”, an affordable complementary health protection solution distributed through French municipalities. Serving over 32,000 customers, this channel distributes individual health coverage, dependency cover and funeral insurance adapted for retirees, microentrepreneurs, and rural inhabitants. - Protecting our clients’ critical productive assets, such as shops, motorbikes, and crops, to sustain their families’ livelihoods (Property & Casualty products) - 42% of customers (8.6 million)

Property & Casualty products are vital to secure customers’ main source of income and sustain their livelihoods. These products provide business owners with emergency cash if business-related assets are damaged due to fire, natural disasters or other incidents.

In line with AXA EssentiALL’s efforts to encourage inclusive insurance distribution through postal networks, AXA Spain’s partnership with Correos, a national postal service, leverages their extensive distribution network of 8,500 post offices across the country to deliver affordable insurance solutions, notably home and motor. This reaches 26,000 customers typically unserved by traditional insurance - including those in rural communities. - Developing tailored product bundles against multiple risks for clients (Bundled products) - 8% of customers (1.7 million)

Based on customers’ needs, AXA EssentiALL designs solutions that protect customers against a combination of risks.

To cover individuals in rural and hard-to-reach areas, AXA has been partnering with CNAAS in Senegal since 2017, starting with a parametric insurance program for cotton, then expanding to the Fagaru inclusive solution, which provides comprehensive health, life and accident coverage. Distributed via cooperatives and village leaders, it currently covers 300 smallholder farmers.

Of policies in force

AXA EssentiALL recognizes that providing inclusive insurance solutions is not only about the economic compensation, but also about accompanying customers throughout their insurance coverage period, to provide additional services and enhance the value provided to these groups. For instance, to support microentrepreneurs in France, AXA partnered with financial sector stakeholders under the ‘Plus 1’ initiative to develop a solution helping them hire their first employee by - combining a digital recruitment platform, personalized coaching and local partnerships.

As a business dedicated to social impact, AXA EssentiALL strives to provide affordable, attractive and accessible products to underserved communities. Our ambition is to strengthen their financial resilience and support sustainable growth, even in the face of unexpected events.

As part of our impact measurement framework, AXA EssentiALL products are assessed using an internal tool that evaluates key dimensions of customer-centricity. This includes enhancing the claims experience, simplifying documentation requirements, enabling advance partial claim payments, and ensuring that claims and complaint mechanisms are transparent and easily accessible through multiple channels. There are efforts in place to collect social indicators to the extent possible. This evaluation informs product improvements and is a first step toward measuring the effects insurance can have within communities.

This evaluation informs product improvements and is a first step toward measuring the effects insurance can have within communities.

In addition, we work with partners to conduct impact measurement research. Collaborating locally, we reach customers directly to understand how our solutions support their household finances against unexpected events, how they would cope with or without insurance, and how we can foster an insurance culture.

Contributing to a Fair and Inclusive transition

Populations living on modest incomes face increasing risks due to the impacts of climate change, coupled with the rising costs of climate adaptation. Farmers are losing their crops, fishermen are getting injured during extreme weather events, and individuals are struggling to work in extreme heat. All of these factors result in lost income. It is estimated that more than 100 million people will be pushed into extreme poverty by 2030 due to climate change, while more than 200 million people could be displaced by more frequent and severe climate disasters.

The impacts of the increasing frequency and intensity of extreme weather events are disproportionately borne by those living on modest incomes, who have little disposable income and adaptive capacity in the aftermath of an event.

The UN estimates that over 100 million people could be pushed into extreme poverty by 2030 due to climate change, while more than 200 million people could be displaced by climate disasters.

Jean Jouzel

Previous Vice-President of the GIEC (Group 1)

One of the first consequences of climate change is increasing inequalities globally.

AXA’s vision is to support the transition to a low-carbon and less resource-intensive economy that also fosters inclusion, resilience, and climate adaptation, including for modest-income populations. By helping individuals and businesses cope with shocks, insurance is an important tool which builds resilience to bring about a fair and inclusive transition globally.

We partner closely with our colleagues at AXA Climate to develop and distribute parametric insurance, which provides much-needed payouts following extreme weather events. In Dakar, AXA Senegal issued a policy to protect a vulnerable neighbourhood, Pikine, against flooding events. Payouts from the policy are triggered following a flood with the payment to be used by the city municipality for recovery and adaptation costs.

A strong leadership voice

For inclusive insurance to effectively contribute to sustainable development, cooperation is needed among a range of public and private actors to find and offer new ways to manage risks. AXA EssentiALL partners with organizations and consortia that share our vision and values and is active in the financial inclusion community. Its partners include:

Related content

- Insurance Development Forum (IDF), where AXA EssentiALL co-chairs the Inclusive Insurance Working Group,

- Microinsurance Network (MiN), where it supports the ‘Landscape of Microinsurance’, which in 2025 released the Microinsurance Data Hub, a publicly available repository of raw data and publications of inclusive insurance around the world,

- World Bank’s CGAP (Consultative Group for Assisting the Poor), where AXA is a private sector strategic partner, advising on projects and research to better ensure the financial health of underserved customers,

- and Universal Postal Union (UPU), currently in the second phase of its partnership to promote inclusive insurance distributed via postal networks worldwide through the Postal Insurance Technical Assistance Facility (PITAF), also with CNP Assurances and other partners.

Governance

AXA EssentiALL, as the dedicated business unit in charge of executing AXA’s commitment to financial inclusion, reports to the Deputy General Secretary and Global Head of HR of the Group. Its performance is overseen by the Inclusive Insurance Steering Committee set up with key AXA Management Committee members. The Compensation, Governance, & Sustainability Committee reviews, at least once a year, the Group’s sustainability strategy (including AXA EssentiALL’s ambition and performance) as well as material sustainability-related commitments disclosed publicly and reports to the Board of Directors in this regard.

On top of these efforts, AXA EssentiALL is committed to AXA's strong Code of Ethics. AXA’s code of conduct includes, for example, a commitment to never providing false information to clients, business partners, and competitors. Through these commitments, we ensure customers are treated fairly and professionally, limiting aggressive sales techniques, and promoting responsible practices.

Since 2024, AXA EssentiALL’s strategy was selected as one of the 19 sustainability topics deemed material for AXA (Impacts, Risks, and Opportunities i.e. IROs) as part of AXA’s first Corporate Sustainability Reporting Directive (CSRD) exercise, reinforcing AXA’s long-term public commitment to financial resilience. It is considered to have a positive impact on closing the protection gap for populations that are un- or under-served by insurance products and services. To reflect the social component of the AXA EssentiALL business, the selected indicator for this IRO corresponds to the number of customers served by inclusive insurance solutions.

Contacts

AXA EssentiALL

Contact Email